Documents Required for F&O Income Tax Audit

Proper documentation plays a crucial role in the successful completion of an F&O Income Tax Audit. Traders engaged in Futures & Options transactions are required to maintain and provide various financial and trading records to ensure accurate turnover calculation, profit and loss assessment, and compliance with applicable tax provisions. The documents required for an F&O income tax audit generally include broker statements, trade reports, contract notes, bank statements, PAN details, previous income tax returns, and other supporting financial records. Maintaining complete and accurate documentation helps facilitate a smooth audit process, reduces the risk of reporting errors, and ensures compliance with the requirements of the Income Tax Act.

Need Help with Audit Documentation?

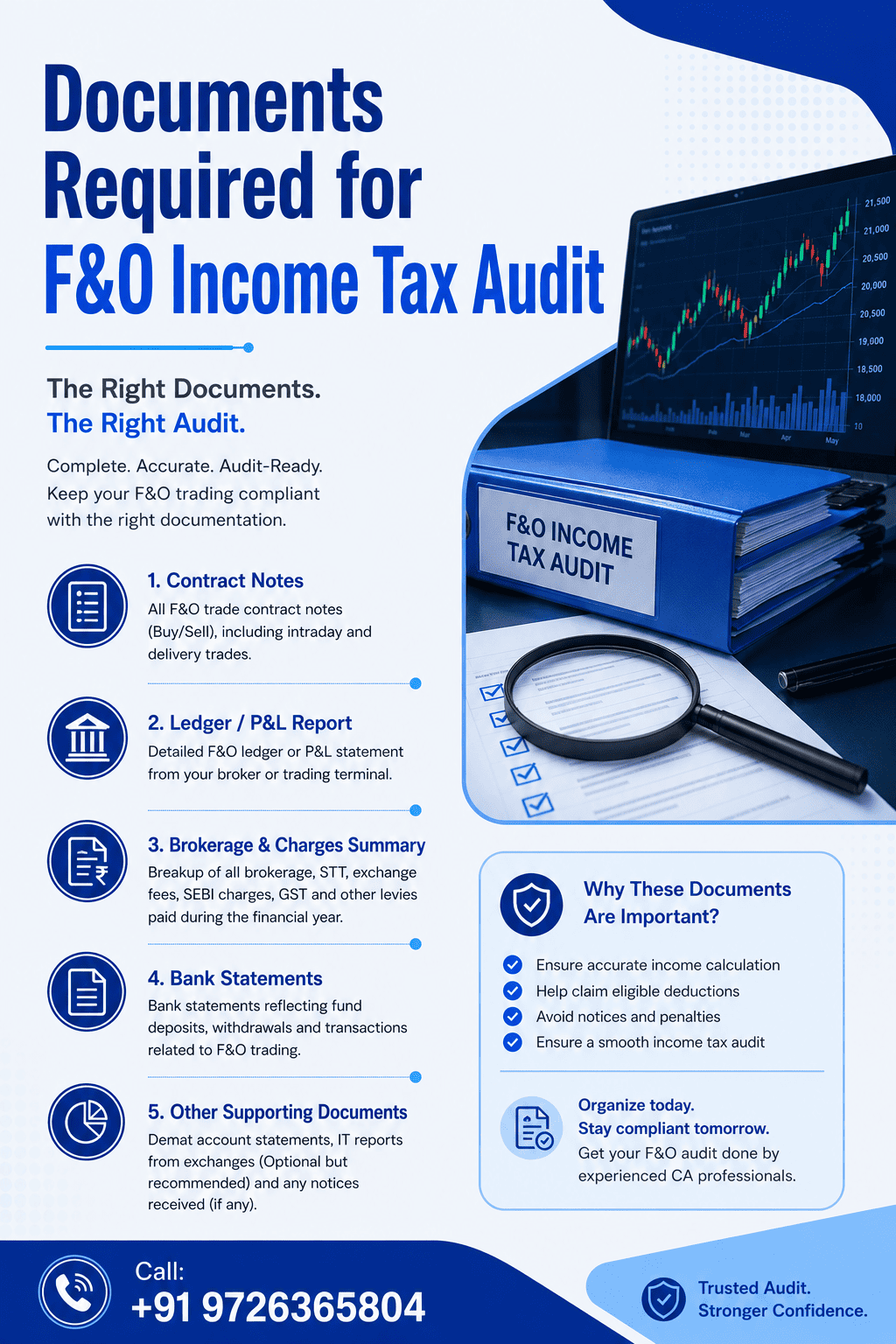

Required Documents for Futures & Options Tax Audit

To ensure accurate turnover calculation, tax audit compliance, and timely filing of your Income Tax Return, please keep the following documents and information ready:

- PAN Card & Aadhaar Card

- Bank Account Details & Statements

- Broker Ledger Statement

- F&O Transaction Statement

- Profit & Loss Report (Broker)

- Capital Gain / Tax Report

- Demat Holding Statement

- Investment Details

- Trading Expense Details

- Other Income Details (if any)

Financial Documents Required for Tax Audit

Financial documents play a crucial role in the Income Tax Audit process as they help the auditor verify the accuracy of the financial statements and assess compliance with the provisions of the Income Tax Act. Businesses and professionals undergoing a tax audit under Section 44AB must maintain and provide complete financial records for the relevant financial year.

The following financial documents are generally required for a tax audit:

Profit & Loss Account

Balance Sheet

Trial Balance

Cash Book and Ledger Accounts

Bank Statements for all business accounts

Sales and Purchase Registers

Expense Vouchers and Bills

Debtors and Creditors Statements

Fixed Asset Register

Loan and Investment Statements

GST Returns and Reconciliation Statements

TDS/TCS Records and Tax Payment Challans

These documents enable the tax auditor to verify business transactions, assess taxable income, identify discrepancies, and ensure that the financial records accurately reflect the business’s financial position. Maintaining organized and up-to-date financial documents not only simplifies the audit process but also helps avoid penalties, notices, and compliance issues during tax assessments.

Books of Accounts Required for Income Tax Audit

Proper maintenance of books of accounts is essential for businesses and professionals subject to an Income Tax Audit under Section 44AB of the Income Tax Act. These records provide a detailed account of all financial transactions and help the tax auditor verify the accuracy of income, expenses, assets, liabilities, and tax compliance.

The following books of accounts are generally required during a tax audit:

Cash Book

General Ledger

Journal Register

Purchase Register

Sales Register

Bank Book

Petty Cash Book

Inventory or Stock Register

Debtors and Creditors Ledger

Fixed Asset Register

Expense Registers and Supporting Documents

Payroll and Salary Records (if applicable)

These books of accounts help the auditor examine the financial activities of the business, reconcile transactions, and ensure that the reported income and expenses are supported by proper documentation. Accurate and regularly updated accounting records also reduce the risk of errors, tax disputes, penalties, and scrutiny from the Income Tax Department.

Businesses should maintain these records throughout the financial year and retain them for the prescribed period as required under the Income Tax Act. Proper bookkeeping not only facilitates a smooth tax audit process but also provides valuable insights into the financial health and performance of the business.

Information Included in Ledger Accounts

Ledger accounts serve as the foundation of a business’s accounting system by providing a detailed record of all financial transactions categorized under specific accounts. During an Income Tax Audit, ledger accounts help auditors verify the accuracy of financial records, identify discrepancies, and ensure compliance with tax regulations.

A ledger account typically includes the following information:

Date of each transaction

Transaction description or narration

Voucher or reference number

Debit and credit entries

Opening and closing balances

Details of customers, suppliers, or related parties

Expense and income classifications

Tax-related entries, including GST and TDS adjustments

By reviewing ledger accounts, tax auditors can trace individual transactions, reconcile balances with supporting documents, and confirm that all income and expenses have been properly recorded. Well-maintained ledger accounts also facilitate the preparation of financial statements, tax returns, and audit reports.

Businesses should regularly update and reconcile their ledger accounts to ensure accuracy and transparency. Proper ledger maintenance not only simplifies the Income Tax Audit process but also helps in identifying financial irregularities and improving overall financial management.

Importance of Maintaining Accurate Records

Maintaining accurate financial records is essential for businesses and professionals undergoing an Income Tax Audit under Section 44AB of the Income Tax Act. Proper record-keeping ensures that all financial transactions are correctly documented, making it easier to prepare financial statements, calculate taxable income, and comply with tax regulations.

Accurate records help tax auditors verify the authenticity of income, expenses, assets, liabilities, and tax-related transactions. They also reduce the likelihood of errors, omissions, and discrepancies that could lead to penalties, notices, or additional scrutiny from the Income Tax Department.

Some key benefits of maintaining accurate records include:

Simplifies the Income Tax Audit process

Ensures compliance with tax laws and regulations

Supports claims for deductions, exemptions, and depreciation

Helps identify and correct accounting errors promptly

Improves financial transparency and business decision-making

Facilitates smooth preparation of financial statements and tax returns

Reduces the risk of tax disputes and assessments

Businesses should maintain updated books of accounts, supporting invoices, bank statements, tax records, and other financial documents throughout the financial year. Consistent and organized record-keeping not only ensures a hassle-free tax audit but also strengthens the overall financial health and credibility of the business.

Turnover Calculation Documents for F&O Tax Audit

These are documents used to calculate and verify F&O turnover for income tax purposes. They include:

Broker P&L Statement

Tax P&L / Tax Report

Trade Book or Order Book

Contract Notes

Ledger Statement

Annual Transaction Summary

Bank Statements

These documents help determine F&O turnover, verify profit/loss, and assess whether a tax audit is applicable under the Income Tax Act.

Download the Complete F&O Tax Audit Document List

Download our complete F&O Tax Audit Document List to ensure you have all the necessary records ready for a smooth and hassle-free audit process.

Common Mistakes in Bookkeeping During Tax Audit

One of the most common challenges faced during an Income Tax Audit is inaccurate or incomplete bookkeeping. Many businesses fail to record transactions regularly, misclassify expenses, overlook supporting documents, or neglect bank and GST reconciliations. These errors can create discrepancies in financial statements and make it difficult for auditors to verify the accuracy of the records. Inadequate bookkeeping may also lead to incorrect tax calculations, delayed audit completion, and potential compliance issues under Section 44AB of the Income Tax Act. To ensure a smooth tax audit process, businesses should maintain updated books of accounts, preserve all financial documents, and perform regular reconciliations throughout the financial year. Proper bookkeeping not only helps meet statutory requirements but also improves financial transparency and supports informed business decision-making.